یہ بھی دیکھیں

25.05.2026 10:30 AM

25.05.2026 10:30 AMGlobal stock markets ended last week on a positive note, showing solid gains. The S&P 500 extended its longest weekly winning streak since December 2023, rising 0.4%. Asian and European markets also posted upward momentum, despite continuing uncertainty related to the conflict in the Middle East.

Recent trading sessions were marked by reports of a possible agreement between the US and Iran, which in turn increased volatility in oil and bond markets. Over the weekend, while markets were closed, Trump said there was "significant alignment" and that an agreement to resume shipping through the Strait of Hormuz would be announced soon. The Iranian side also confirmed progress in talks, although significant disagreements over Iran's nuclear program and sanctions relief remain. Iran is expected to resume operations at the Siam port in exchange for the US lifting its naval blockade. Sources on both sides emphasize that the agreement is a framework and does not address Iran's nuclear or missile programs. Secretary of State Rubio and President Trump expressed caution, stressing that "you can't do a nuclear deal in 72 hours on a napkin" and that the US "will not rush into a deal."

If this de-escalation trend continues, demand for risk assets should rise, and oil prices could correct significantly lower. On Monday morning, Brent was trading below $100 per barrel for the first time in two weeks. Against the backdrop of falling oil prices, EUR/USD opened higher and German bond futures traded with lower yields.

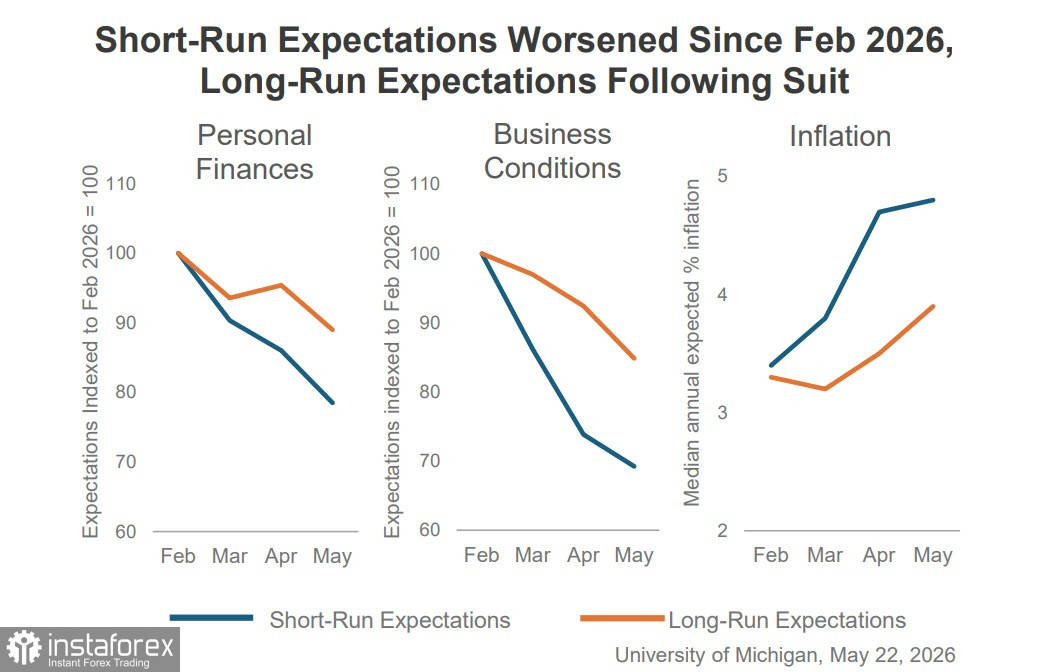

In May, the University of Michigan's consumer sentiment index fell to a record low of 44.8 points. Households are increasingly worried about the inflationary effects of the conflict in the Middle East. A key factor behind the drop appears to be rising fuel prices: the price of gasoline in the US jumped to $4.55 per gallon, up 53% since the end of February.

Federal Reserve Board member Christopher Waller, who had previously advocated cutting interest rates—believing that inflationary pressure from trade tariffs would be temporary—has now revised his stance. He said that rising inflationary risks related to the conflict with Iran call into question the wisdom of further rate cuts. In his view, the Fed should hold rates at current levels for the foreseeable future and be prepared to raise them if inflation remains elevated. Waller's comments have already had a noticeable impact on market expectations. By December of this year, a 25 basis-point rate hike is now fully priced in, whereas earlier in the session, that probability was only 18 basis points, and a second hike could occur as early as March 2027.

We are poised to believe that forecasts of further dollar weakness will be revised. A likely agreement with Iran would trigger a sharp increase in demand for risk assets and lead to a decline in the dollar index, but over the long term, the dollar is more likely to continue strengthening.